Dr. Naresh Bana

The Adani Group’s wind power project in Mannar, Sri Lanka, has a planned capacity of 250 megawatts (MW). This project is part of a broader investment in renewable energy by Adani group in Sri Lanka, with expected completion by 2025. This initiative aims to support Sri Lanka’s renewable energy goals and create up to 2,000 local jobs during construction and operation- Located in Mannar District, Northern Province, Sri Lanka. Estimated investment: $250 million. It is one of the largest under development wind power projects in Sri Lanka.

As soon as the new government took office varied types of views are being propagated. As happens in any democracy the most vocal voices are those raising questions on the large projects planned by the outgoing office bearers. While it can’t be denied that there may be valid reasons for review and deeper scrutiny of projects awarded earlier or under implementation, due care must be exercised lest the investment climate is impacted. Extra caution is advised considering the economic situation of 2022 and subsequent positive growth of economy; which needs to be maintained. In any case any illegality and any project against the National interests of Sri Lanka has no place on any Government’s agenda. Recently it was argued in media that Adani’s wind power project in Mannar should be cancelled for reasons ranging from procedural irregularities to excessive PPA prices to lack of alignment to global standards to environmental concerns and long-term National interests. In total five major reasons have been cited against the project. On the other hand a detailed study and research based output tells another side of story which must be told to enable readers to form their own opinion as it matters to them the most.

The Process Followed for Adani Project.

Adani Green Energy Limited (AGEL) promoted wind power project was granted approval by Cabinet Appointed Management Committee on Investments (CAMCI) under the Fast tracking of Investments”, a process formulated under laws of Sri Lanka. Thereafter, Cabinet Approval was granted to enter into MOU with AGEL. Ministry of Finance’s notification states that in cases where CAMCI’s decision prevails, there is no need for tendering process. The Project complies with the provisions of Electricity Act of Sri Lanka. Public Utilities Commission (PUCSL) has also granted approval to procure power from AGEL. This project is also included by PUCSL in their Long-Term Generation of Electricity Plan (LTGEP 2023-24). The Government of Sri Lanka has in recent times received a single bidder with single location based Renewable Energy (RE) proposals and approved that too. A similar process has been followed for AGEL as well. Proposal also complies with the recent MOU signed between India and Sri Lanka on Renewable Energy Co-operation” allowing both private & public sector participation from both Countries.

PPA Pricing of Electricity Generated by The Adani Project.

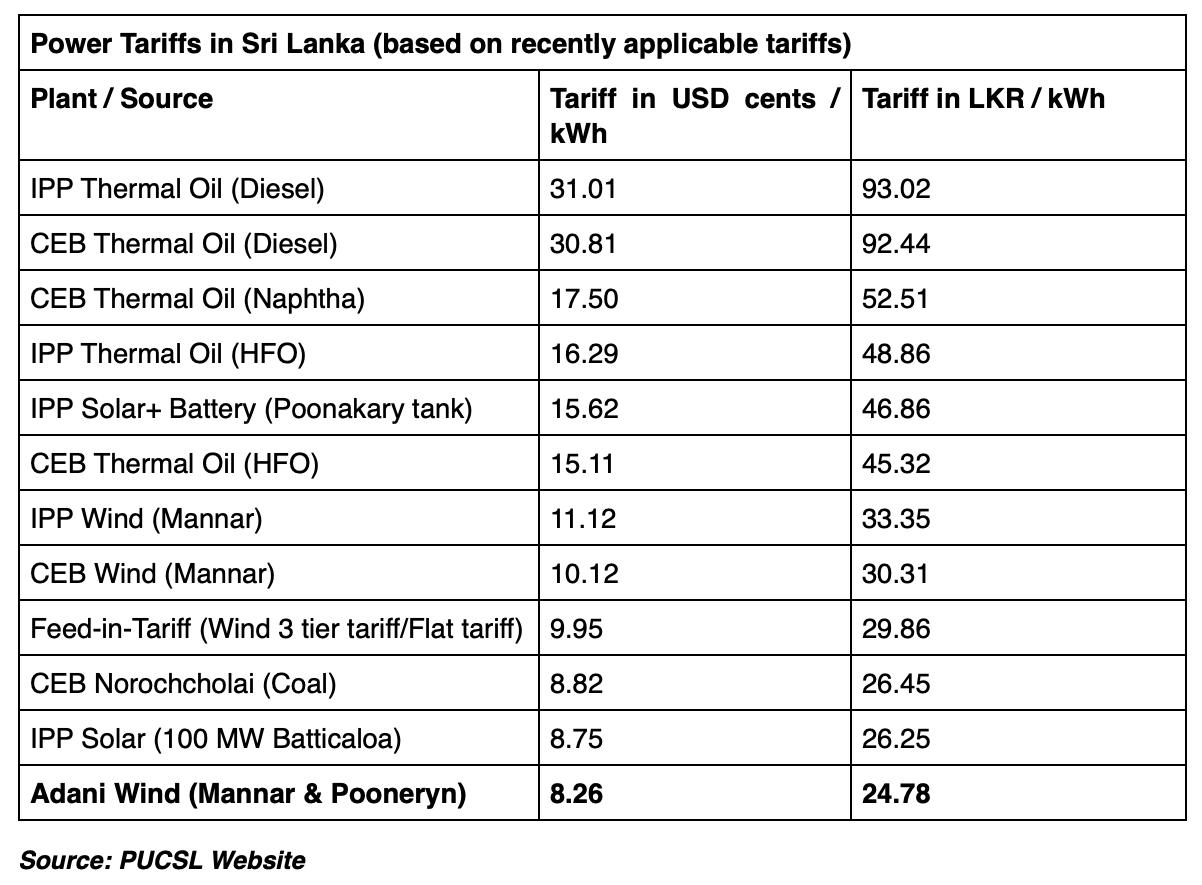

It is alleged that AGEL has been given favorable treatment and excessive price per unit has been granted to Adani Project in Mannar and Pooneryn . In fact, the wind tariffs of Adani’s project at Mannar and Pooneryn are the lowest in the country. Below is the data from PUCSL website which is visible to anyone and should be referred to while making any argument to the contrary:

It is evident that the PPA rates agreed for Adani Project are indeed lowest among the projects listed in the table above. It further demolishes the theory of excessive payments of billions of USA dollars over the project life cycle. On the contrary, the timely investment is likely to add to the power availability of the country and help manufacturers and households alike in times of scarcity and high costs of power coming from fossil fuel sources. Needless to say it will bolster the investment climate of Sri Lanka.

Comparison with Global Standards.

An effort seems to have been made to draw comparison based on Levelized Cost of Energy (LCOE), a widely acknowledged benchmark for pricing of PPAs globally. Opponents of the Adani Project state that LCOE for wind projects worldwide has declined steadily over the years, a trend documented by the International Renewable Energy Agency (IRENA). Drawing upon such perception they argue that AGEL project at $ 0.08/Kwh is excessively priced. A quick look at PUCSL website again defeats such position as there is an IPP in Mannar and CEB project also in Mannar where PPAs are signed for $ 0.1112 and $ 0.1012 per unit, respectively. In fact, the Adani Project PPA energy pricing confirms the IRENA trend of lowering of the tariffs over the years. Additionally, AGEL pricing is in line with the CEB power procurement rates published over a period of time for purchasing power based on Standardised PPAs. Comparing with US Dollar rates of PPAs entered into by Adani Group in India may be neither lawful nor justified as the two sovereign countries have their own policy and investment paradigm, different than each other.

Environmental Concerns.

Mannar project site is claimed to be problematic as it harbours the habitat for migratory birds, making it sensitive to large projects. Alternative sites have been suggested and some data from a foreign source has been quoted. Those who make such arguments may like to answer that if Mannar site is problematic then why is another 100 MW wind IPP implemented right there? Why is the 50 MW tender being conducted there? Why is small wind IPPs 5 MW size approved there in same Mannar region. It also needs to be appreciated that the Adani project has undergone extensive EIA process (similar to that of CEB’s 100 MW) and doesn’t fall into any of the crucial habitats as mentioned, may be inadvertently.

Larger Implications for Economic Development.

The arguments made by critics of Adani wind project in Mannar and Pooneryn are primarily based on their misplaced perception of procurement procedure and pricing followed by the previous governments. Both of these are untrue as presented in this piece above. Therefore, it is worthwhile to look at probable scenarios when such investment is not available to Sri Lanka. Firstly, the absence of almost $ 250 million of Foreign Direct Investment (FDI) may dampen the ‘barely breathing to life’ investment climate of Sri Lanka. Secondly, Sri Lanka may not be able to reduce power tariffs and consumers may continue to pay more by almost $ 80 plus million per annum due to continued dependency on fossil fuel-based generation. Thirdly, it may set a difficult precedence by opening the PPAs of such investors and others approved earlier? Fourthly, the resultant litigations and insurance claims will further push up the cost of project finance for Sri Lanka thereby increasing the project costs. Lastly, the investment and project risk profile of the country will become more complex, all to the detriment of future FDI inflows.

Reviewing and relooking at the big projects after assuming office is the right of any government. It is prudent to ensure such review is based on the merits of the case and not driven by narrative, which is so easy to be manipulated in the current age of social media. It is imperative to appreciate that large publicly listed corporations are not only subject to the laws of the host country where they take up projects but also face repeated scrutiny in the hands of stock market watchdogs and regulatory authorities in their home country and worldwide. An emerging economy like Sri Lanka which faced a complex situation not too far back in past may be well advised to undertake only an independent merit-based review of all those foreign investments and infrastructure projects which may have appeared to them in a different shade in run up to Presidential elections.