A comprehensive new bill aimed at overhauling Sri Lanka’s direct tax regime was published in the Gazette Extraordinary on 20 February 2026 and issued by the Minister of Finance, Planning and Economic Development on Tuesday (24 Feb).

The proposed legislation, which seeks to amend the Inland Revenue Act, No. 24 of 2017, introduces a series of significant changes once it is enacted through the constitutional legislative process.

According to a Tax Flash released by KPMG in Sri Lanka, the amendments are designed to broaden the tax base, enhance compliance, and offer targeted relief, impacting individuals, corporations, investors, and a wide array of service providers.

Key proposed measures include:

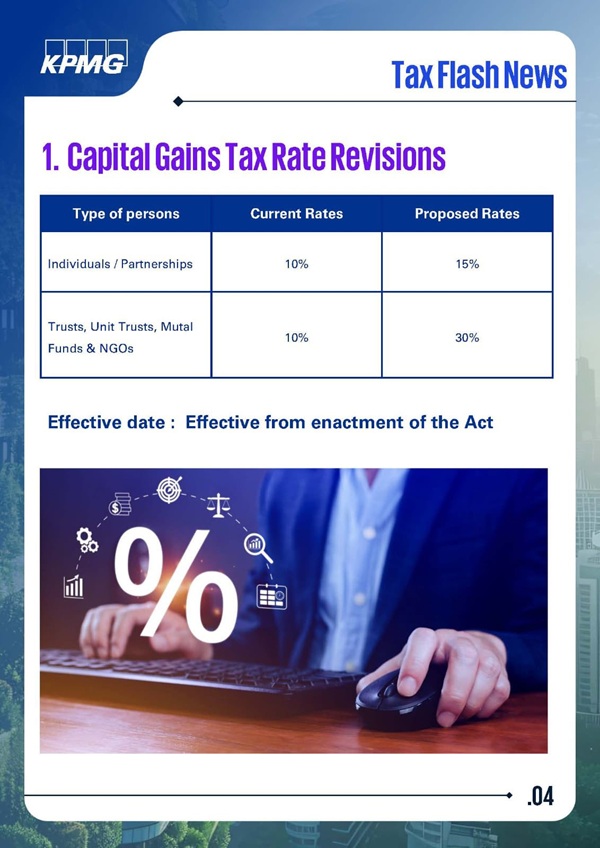

- Revision of Capital Gains Tax Rates: Capital Gains Tax (CGT) rates are set to increase from the date of enactment. For individuals and partnerships, the rate will rise from 10% to 15%. A more substantial increase is proposed for trusts, unit trusts, mutual funds, and NGOs, where the rate will jump from 10% to 30%.

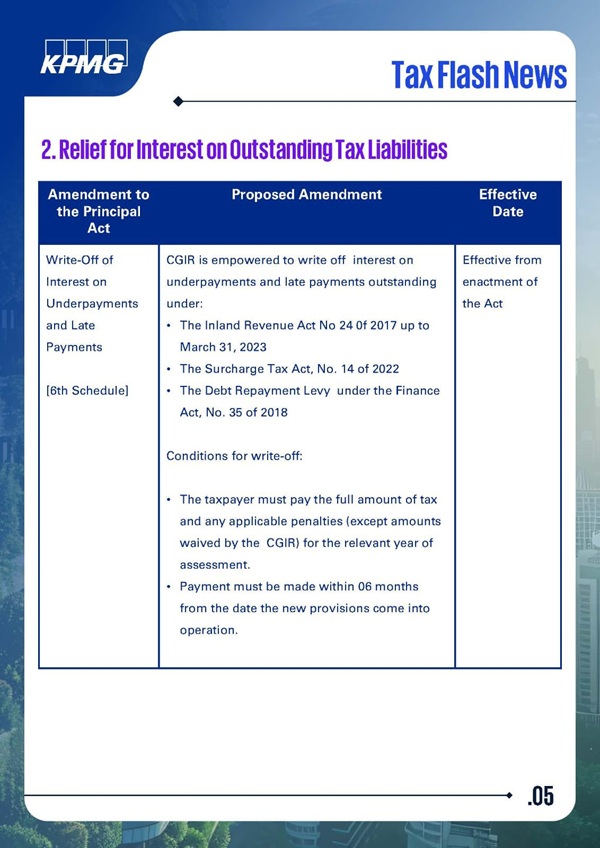

- One-Time Interest Relief on Outstanding Tax: In a move to encourage settlement of old dues, the Commissioner General will be empowered to waive interest accrued on underpayments and late payments up to 31 March 2023. This relief, applicable to liabilities under the Inland Revenue Act, Surcharge Tax Act, and Debt Repayment Levy, is conditional upon the full settlement of the principal tax and any applicable penalties within six months of the Act’s enactment.

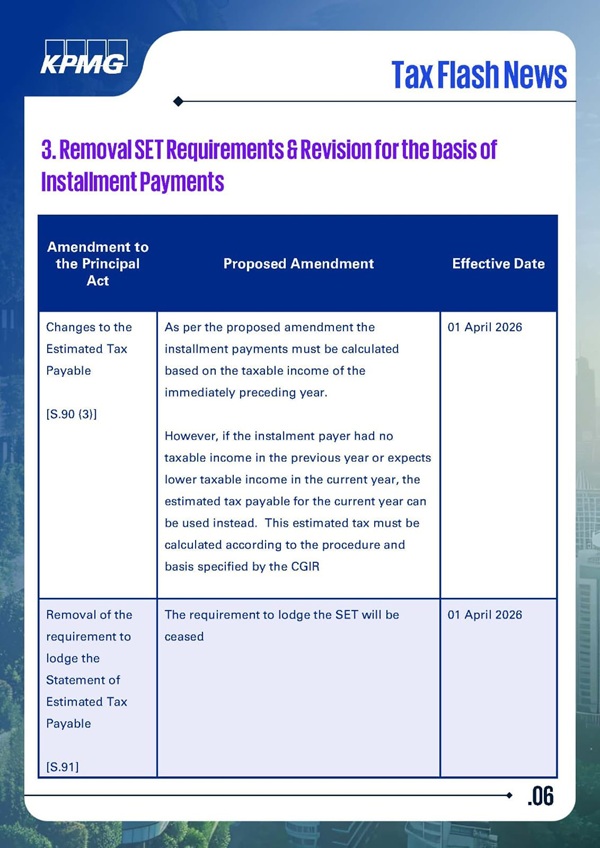

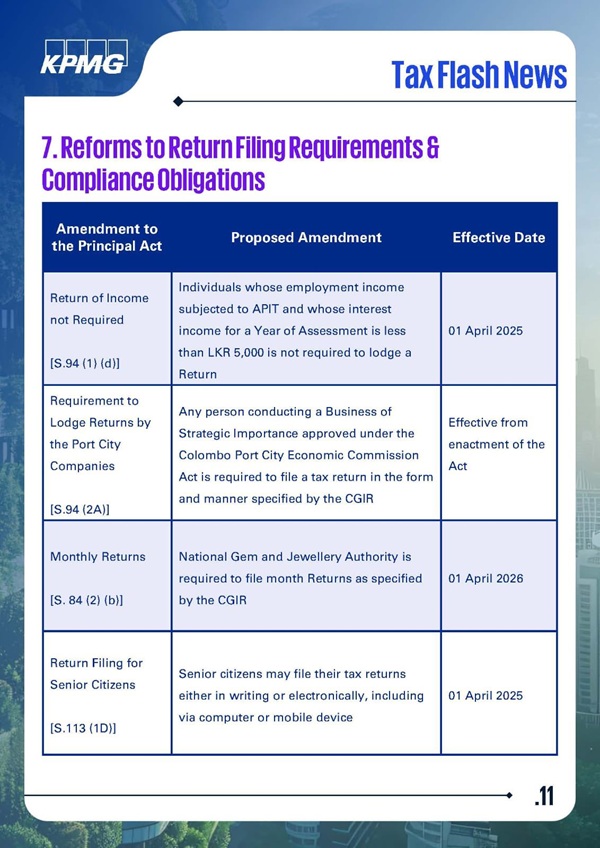

- Simplification of Instalment Tax Payments: Effective 1 April 2026, the process for tax instalments will be streamlined by removing the requirement to file a Statement of Estimated Tax (SET). Instead, instalments will generally be calculated based on the taxable income of the immediately preceding year. Flexibility will be provided for instances where the prior year’s income was nil or where the current year’s income is expected to be materially lower.

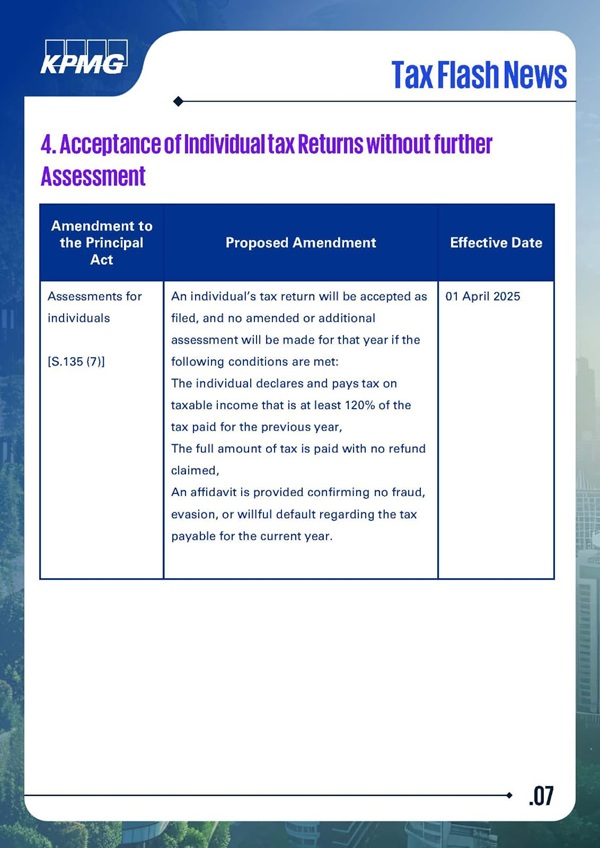

- Acceptance of Individual Returns Without Further Assessment: For the year of assessment commencing 1 April 2025, a new fast-track mechanism will be introduced. Qualifying individuals who declare and pay tax on at least 120% of the prior year’s taxable income, make full payment without claiming a refund, and submit a prescribed affidavit confirming compliance will have their returns accepted as filed, with no amended or additional assessment issued.

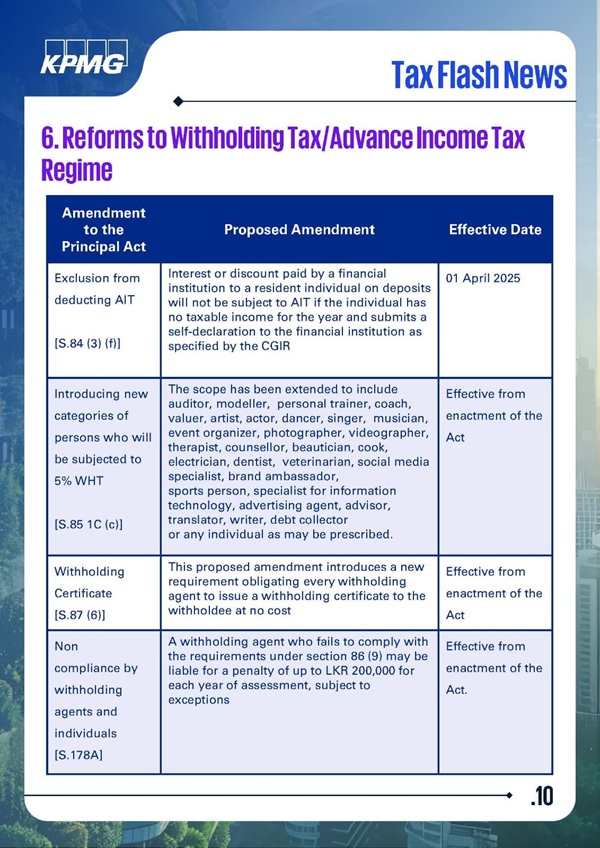

- Expansion of Withholding Tax (WHT) Scope: The list of service providers subject to a 5% withholding tax will be significantly expanded from the date of enactment. The new categories include auditors, valuers, personal trainers, coaches, entertainers, photographers, therapists, beauticians, social media specialists, brand ambassadors, and debt collectors, among others.

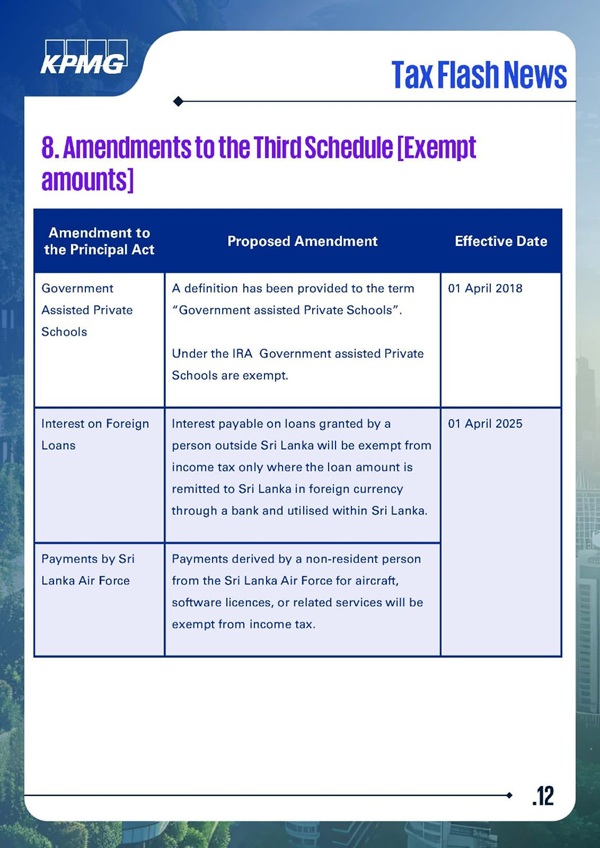

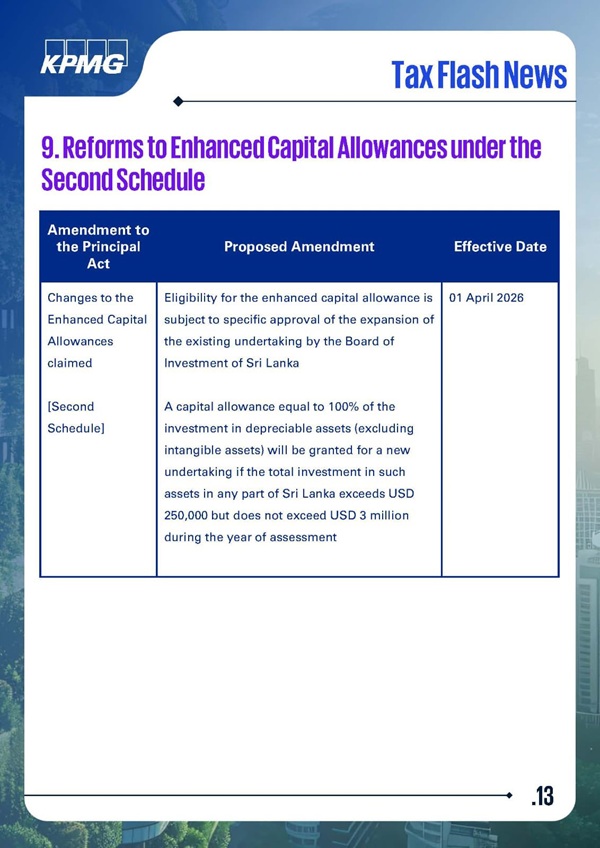

- Other Important Reforms:

- Enhanced capital allowances for qualifying investments, subject to Board of Investment approval.

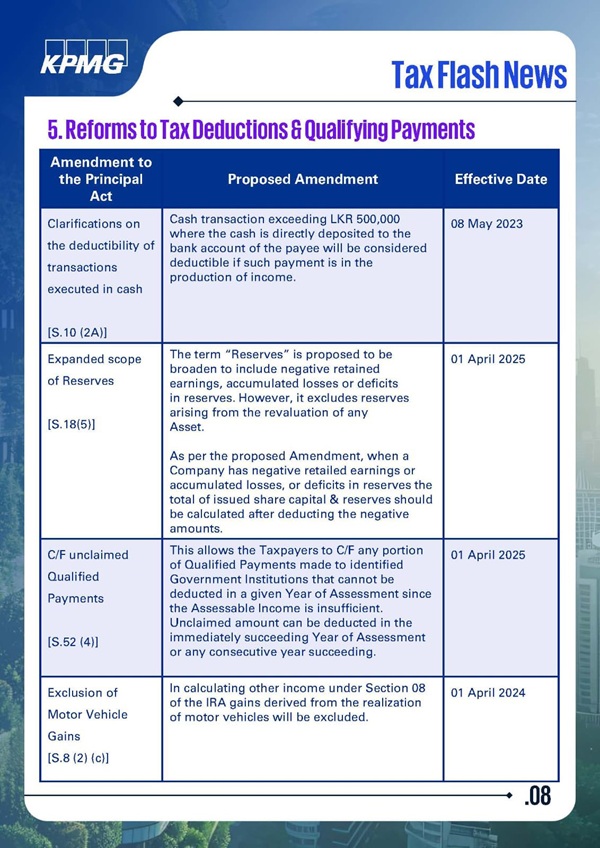

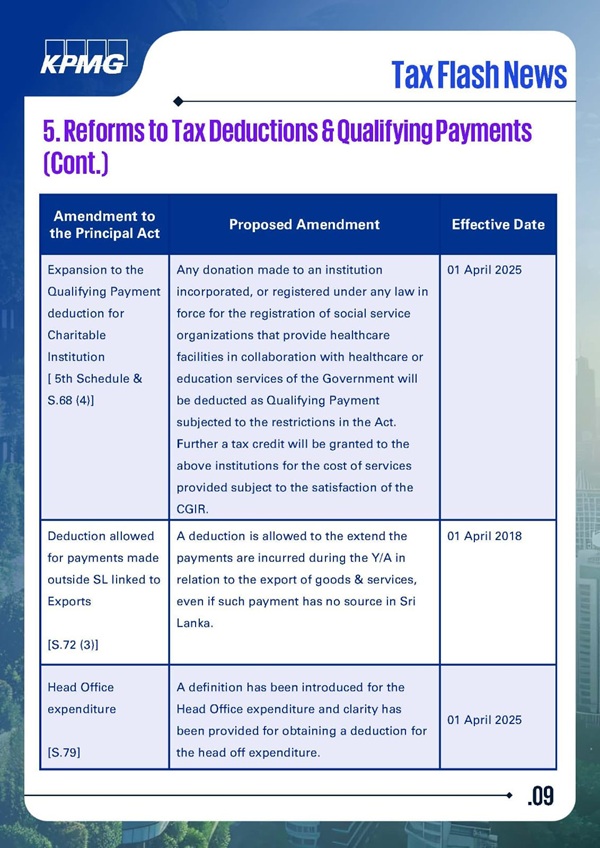

- Updated rules on qualifying payments, deductions, and residency.

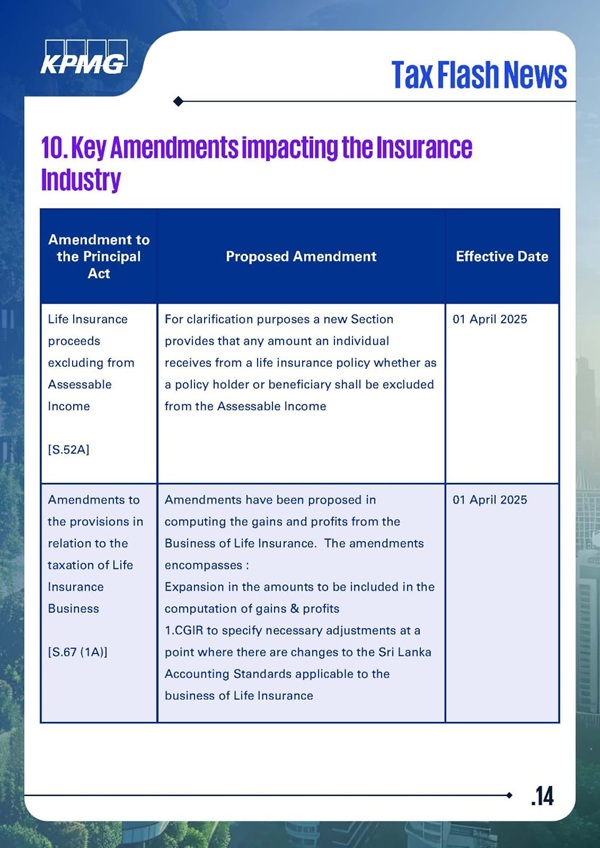

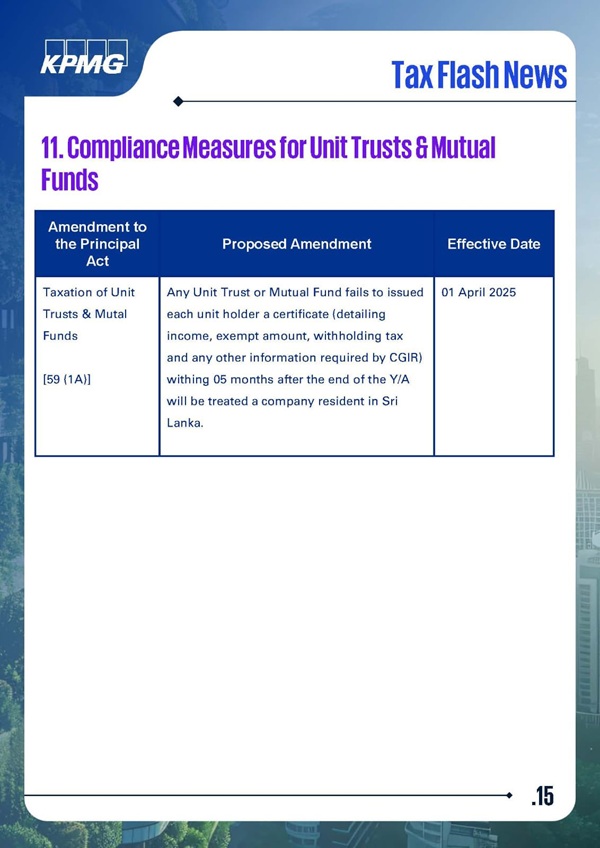

- Specific provisions affecting the insurance sector, unit trusts, mutual funds, and the treatment of salary arrears and cancelled contracts.

- New tax administration and enforcement measures.

The provisions outlined in the bill will only take effect upon enactment and on the respective dates specified in the final Act.

KPMG Sri Lanka recommends that businesses, investors, high-net-worth individuals, and tax professionals review the proposed changes in detail to assess their potential impact. (Newswire)